Leasing & Asset Finance: Relevance in Circular Growth Business Models

Leasing & Asset Finance may not be real definers of Circular supply-chain and manufacturing innovation for a Circular economy. However, our industry has a key opportunity to enable funding for these manufacturers/dealerships, and more importantly, to provide lifecycle asset management which is pivotal on all of the potential growth business models in a Circular economy. In the last post, we ended with the potential different growth models in a Circular economy. In this post, we will look at the key elements and strategic options in the Leasing & Asset Finance lifecycle that either directly contributes to, or at the very least influence these growth models.

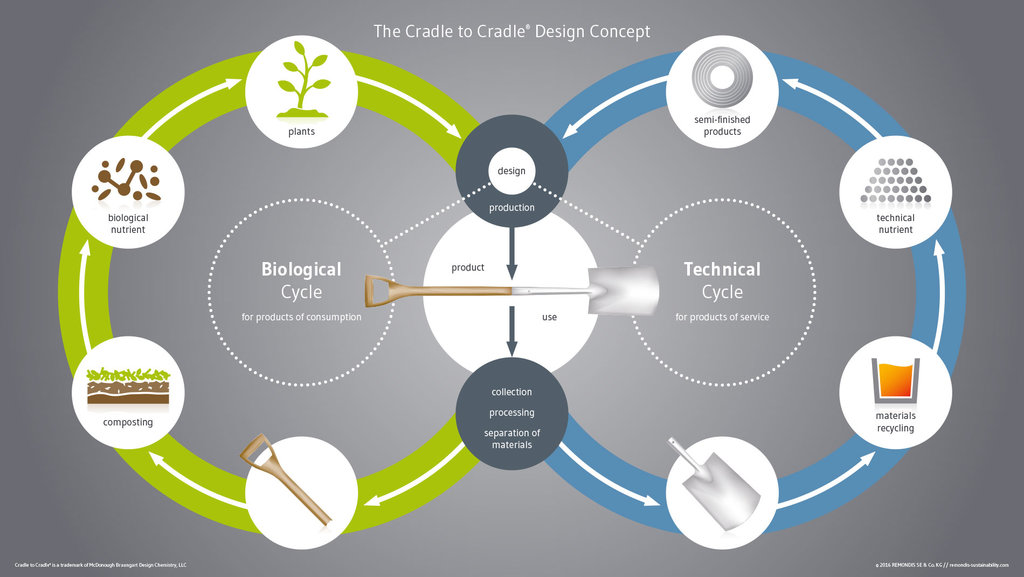

Circular supply-chain & design

Circular supply-chain embraces fully renewable, recyclable or biodegradable inputs (raw materials) as substitutes for linear ones, and this is a key aspect of the circular economy that closes the loop to convert waste into wealth. This particular growth model focuses more on the manufacturing process and key modular design principles such as Cradle-to-Cradle[1], Product passporting[2] holds the key towards usage of right raw materials, and equally importantly, effectively used in the refurbishment, re-manufacturing and recycling process.

Even though this growth model is related to manufacturing, for the Circular supply chain to work, Asset Finance as an industry plays a key partner role on the product life extension and recovery/return channel of the assets. We will look at the product life extension, return channel at a greater depth in separate growth models.

Products manufactured with circular supply-chain & design deeply ingrained in its principles will result in a far better economic life and hence a positive redefinition of its value in the lifecycle. Both economic life and asset’s lifecycle value are key elements for our industry for usage/performance-based financing.

Once the adoption of this model by the manufacturing companies increases, there are some key strategic questions that all Asset Finance companies – but more importantly banks and independent lessors – need to answer as they evaluate their business model:

•Are we a true financing partner working with our vendor/dealer to understand the assets and support asset lifecycle management, or am I just a funder focused on pure deal margin?

•Are we supporting our vendor for an easier financing channel?

•Are we agile in our business and technology to adapt to the changing market demands for the assets and vendors?

The drive towards a usage rather than ownership model demands Asset Finance companies with strong asset lifecycle management capabilities such as Captives, or lessors with a strong vendor relationship management.

Sharing platform

The foundation of the sharing platform is the sharing economy, allowing consumption growth without the need to produce anything new while maximising the utilisation of the asset by having multiple customers sharing the asset.

There is significant overlap between a Sharing economy and a Circular economy, such as the extension of product life through better resource utilisation (in turn incentivising the product design for a longer lifecycle). However, the fundamental difference is the social component; community building is a crucial part of the sharing economy, and this is called “collaborative consumption”.

Leasing and Asset Finance, at least in their current form, probably have the least direct impact on a Sharing platform business model than the other business models discussed. That said, there are a couple of areas in which asset finance could contribute towards a sharing economy:

1. Leasing / Asset Finance can help companies that have a sharing platform business model. Companies like these lease their assets (e.g. Zipcar lease their auto fleet), and in turn used for a sharing model. As more companies bring in the sharing economy for different asset classes, we could see Leasing / Asset finance as a driving force behind it. At the same time, though, there is a need for Leasing / Asset finance to come out beyond the traditional way of funding & rigid lease product approach, and start to offer pay per performance to truly flexible and adapt to these businesses.

2. In B2C leasing, some asset classes such as Automobiles & Real Estate, lessors enter into a contract agreement with multiple lessees for the same asset based on usage. The concept of co-lessee in Leasing (though currently not that prominent due to its legal and regulatory uncertainty) is probably a direct relevance in a sharing economy. Especially in Automobiles, when advancements such as a driverless technology become a practical reality, adoption of leasing between multiple lessees could be controlled better by digitisation as usage terms enforced on a contract could be controlled better by the smarter asset.

“Smarter Assets and Digitisation could drive usage/performance/outcome based leasing across lessees for the same asset.”

Having looked at the Circular supply chain/design and the sharing economy, the circular business models that follow are the ones where Leasing & Asset Finance have the most direct impact, and this is where our focus will be on the future blog posts in this series.

Product life extension

Product life extension

As more manufacturers design their products to be more modular & durable for a circular economy, a product’s useful life and maximising the profitability of each asset become more important; and this is where Leasing & Asset Finance can have the biggest impact on the Circular economy.

Key areas for product life extension in the context of Leasing & Asset Finance are:

•Preventative & Corrective maintenance

•Lease extensions & modular upgrades

•Re-Leasing to maximise the useful economic life

Preventative & Corrective maintenance

In Leasing, Asset maintenance throughout the lifecycle can either be done directly by the Asset Finance companies (such as Asset-intensive lessors who have the skills and capability) or by the manufacturers/vendors through a close and deep partnership with the Asset Finance companies. As lessees transform to usage rather than an ownership model, the total cost of ownership shifts towards the manufacturers/Asset Finance companies, making the preventative and corrective maintenance pivotal to protecting the value and life of the asset.

Preventative maintenance ensures that the asset is in its optimal shape throughout its lifecycle, rather than waiting for it to degrade in performance – or worse – break down. Corrective maintenance includes carrying out component upgrades due to performance degradation or asset repairs due to damages. Predominantly in today’s world, this is done through routine inspection and service. However, with the advent of assets becoming truly smarter and digitisation as a whole, Asset Finance companies who have the capability in their business process and technology platforms to manage could see even more gains in maintenance.

Asset-focused lessors who have the skills and capability for maintenance could become the key differentiators in the Leasing space enhancing their profits exponentially as the economic life increases.

Lease Extension & modular upgrades

Providing the lessee still needs the use of the asset, Asset Finance companies can provide contract extensions through either better-priced renewals or modular upgrades and refurbishment so that they can continue to extend their lease.

Re-leasing to maximise the useful economic life

Re-leasing ensures that when a lessee eventually returns the asset, its marketed for re-lease to another customer in ‘used asset’ financing rather than being sold.

Again, like in-life maintenance – Asset refurbishment and management needs after the return is either handled by asset-focused lessors themselves in-house or through partnerships with an external vendor/manufacturer to re-lease to another customer for financing.

Beyond the profits, the most significant benefit for Asset Finance companies with product-life extension business model is the deeper relationship they develop with their vendors and customers.

Recovery & Recycling

With the global competition intensifying and resources becoming more scarce and costly, manufacturers are looking for ways to protect, re-capture and re-use the resources hiding in their production outputs and discarded products. Additionally, we are also paying a lot for the privilege of asset disposal at the end of its life.

Recovery and recycling as a business model are different from pure recycling: Here waste is viewed not as an external problem to be dealt with only by legislation or waste-management entities, but as a resource that is fully integrated into the business model[3].

Leasing & Asset Finance as an industry can serve as a key channel to enable the return of assets, so recovery and recycling can close the loop and allow raw materials back into remanufacturing or as a by-product to manufacturing something else.

There is a reason why recovery & recycling as a business model comes after the product-life extension business model; recovery & recycling should ideally be considered after restoration, refurbishment of the asset to use in its form.

As with other business models, the key to the recovery and recycling business model is the modular design and product passporting as discussed initially in this article. Lessors who are serious about asset lifecycle management understand the competitive edge recovery and recycling holds. Some asset-focused lessors have their recovery & recycling through their in-house refurbishment centres while others might have a buy-back relationship with the manufacturer or have strategic partnerships with specialised vendors.

Product as a service

As usage, performance and outcome become more important, more predictable and more economically viable than ownership for the lessee, assets on the contract are just a small part of the overall financing arrangement.

Asset Finance companies who understand this offer solution financing – beyond just the fundamental lease products – which is the key to the Product as a service (PaaS) model.

A few examples of this below:

•Philips’ lighting as a service

•Siemens’ energy performance contracting

•Managed cloud service (in Technology) – Incorporating infrastructure, software and support

Key differentiators for the Asset Finance companies to handle the product as a service (PaaS) business model is the deeper knowledge of the asset, its usage and vendor relationships combined with the deeper relationships with their customers to understand their industry and its needs.

And this would challenge the true captives to think beyond their parent manufacturer assets and their competition with Asset-intensive independent lessors shifting focus beyond just asset knowledge to industry specialisation combined with deeper customer and vendor relationships.

“What if the customers come with a problem or an outcome for their business for which they needed financing, and they want the Asset Finance company to work out what’s needed to achieve that performance or outcome?, and the customer would be willing to pay for that outcome (not just the assets) over a period.”

Perhaps, we might see more of our industry focusing on Asset management and move into the PaaS arena.

In the next few posts of this blog series, we will look at Asset Lifecycle management case studies conducted through our interviews. Follow us on LinkedIn and Twitter to stay tuned!

__________________________________________________________________________

[1] Cradle-to-Cradle : Sustainability Dictionary. Available: https://sustainabilitydictionary.com/2005/12/03/cradle-to-cradle/ [Apr 8, 2018].

[2] HUNTER, J., -10-16T12:23:02+00:00, 2015-last update, What’s a product passport and can it work for businesses?. Available: http://makeresourcescount.eu/whats-a-product-passport-and-can-it-work-for-businesses/ [Apr 8, 2018].

[3] LACY, P. and RUTQVIST, J.,1982- author., 2015. Waste to wealth: the circular economy advantage. Basingstoke, Hampshire: Palgrave Macmillan.