The CxO Playbook for Deploying AI Agents for Underwriter Decisioning

As pressure mounts to accelerate decisions and reduce operational costs, CxOs in lending and leasing are turning to AI agents to modernise underwriting. These intelligent, goal-driven systems offer more than just automation. They reshape how credit decisions are made, blending speed with control and compliance. This playbook outlines how to strategically deploy AI agents across your underwriting lifecycle, from instant approvals to exception handling, and unlock tangible business value at every stage.

Agents for Automation

The next wave of operational efficiency in lending and leasing is being driven by AI agents that can automate and augment the underwriter decisioning process. Whether you are handling commercial loans, asset finance, or leasing agreements, an AI-powered approach can transform both customer experience and risk management. Here’s how to make it work for your business.

Step 1: Define Your Decisioning Flows

Start by mapping the main credit and lease approval flows in your business. For most organisations, these include:

- Automated Instant Approval: For applications that meet all credit policy criteria, the AI agent can instantly approve, verify legal entities, run AML and KYC checks, perform ID verification, check credit scores, collect and verify documents, and capture e-signatures, all without human intervention.

- Assisted Human Underwriting: For applications that fall outside policy or require further review, the agent gathers all relevant data and presents it to a human underwriter via a unified dashboard. The underwriter can review, request further information, verify documents, and make alternative offers (such as lower loan amounts or requiring additional guarantors).

- Conditional and Staged Approvals: In some cases, you may need staged approvals (e.g., subject to additional collateral or documentation) or conditional offers. The AI agent can manage these workflows, prompting both applicants and underwriters as needed.

- Portfolio and Exception Management: The agent can also monitor existing agreements, flagging exceptions or risk triggers for human review, and automating renewals or extensions where policy allows.

Step 2: Build a Robust Credit Policy Framework

The effectiveness of your AI agent depends on the clarity and completeness of your credit and risk policy. Work with your risk and compliance teams to codify decision rules, exceptions, documentation requirements, and escalation paths. This foundation ensures the agent can automate confidently and escalate only when human judgement is truly required.

Step 3: Integrate Data and Document Sources

Seamless automation requires access to internal and external data sources. Integrate your core systems (CRM, loan management, document storage) and third-party services (credit bureaus, AML/KYC providers, identity verification, e-signature platforms). The AI agent should be able to pull, validate, and store all necessary information in a secure, compliant manner.

Step 4: Design the Underwriter Dashboard

For cases requiring human intervention, the underwriter dashboard is your productivity engine. It should present all relevant application data, risk flags, documents, and communication tools in one place. The agent should ask structured questions, suggest next steps, and enable direct interaction with applicants for clarifications or additional information. Underwriters should be able to approve, decline, or make alternative offers with a single click.

Step 5: Ensure End-to-End Auditability and Compliance

Every action taken by the agent and underwriter must be logged, traceable, and reportable. This is essential for regulatory compliance, audit readiness, and internal governance. Automated workflows should include built-in checks, escalation triggers, and documentation of all decisions.

Step 6: Pilot, Measure, and Optimise

Begin with a controlled pilot in a specific product line or customer segment. Define clear KPIs such as approval turnaround time, manual intervention rates, compliance exceptions, and customer satisfaction. Use these metrics to refine your flows, credit policy, and dashboard features before scaling across the business.

Step 7: Drive Change Management and Adoption

AI agents are only as effective as the people who use them. Invest in training, communication, and support for your underwriters, risk teams, and customer service staff. Address concerns about automation, emphasise the value of human expertise, and position the agent as a partner that frees up time for higher-value work.

Step 8: Scale and Innovate

Once proven, expand the agent’s remit to new products, geographies, or customer segments. Explore advanced use cases such as portfolio monitoring, dynamic pricing, or predictive risk analytics. Continuously review and update your credit policy as market conditions and regulations evolve.

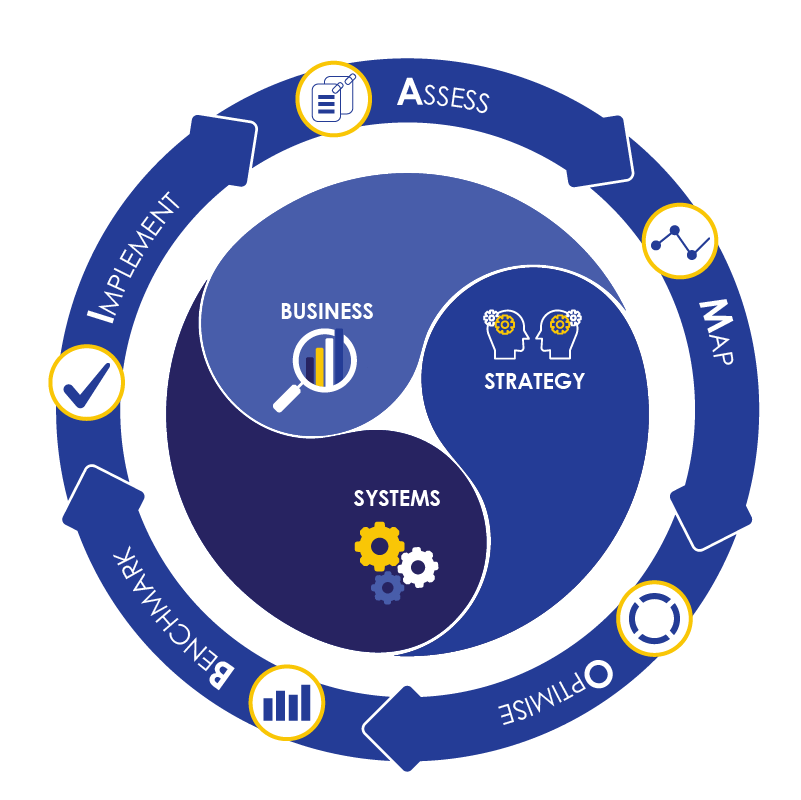

The AMOBI Difference

Implementing an AI agent for underwriter decisioning is not just a technology project-it’s a business transformation. Our AMOBI methodology ensures your solution is tailored to your operating model, risk appetite, and regulatory landscape.

We help you:

- Map and optimise decisioning flows

- Codify and automate credit policy

- Integrate data and systems securely

- Design intuitive dashboards for underwriters

- Deliver measurable ROI and compliance

With deep sector expertise, we guide you from strategy to execution, ensuring your AI agent delivers sustainable value and competitive advantage.

Ready to transform your underwriting with AI? Contact VIP Apps Consulting to start your journey.